Emerging market stocks have had a tough year as global trade tensions and a rising U.S. dollar have crimped growth and made investors wary of investing in these fast-growing economies.

But these worries shouldn’t cloud the longer-term view. The growth of emerging markets is an unstoppable force and the sell-off provides a chance to invest at a cheaper price.

One way to evaluate the growing importance of emerging markets is through the behaviour of the Canada Pension Plan Investment Board (CPPIB). The CPPIB is one of the world’s largest pension pools, with assets worth $366.6 billion as of June 30. It is responsible for investing our CPP premiums and making sure the plan has the money to pay retired Canadians.

The CPPIB plans to have 33% of its assets in emerging markets by 2025, CEO Mark Machin said in the board’s 2018 annual report. That’s just eight years from now. In other words, the CPPIB is betting our retirement security on these markets and sees India as one of three key investment targets, along with China and Brazil.

You may not feel comfortable with a 33% emerging market weighting in your portfolio, but you might consider 5% or 10%. It is something to discuss with your advisor.

India’s size and rapid transformation makes it one of the most compelling emerging market stories. Consultant PricewaterhouseCoopers sees India as the world’s second largest economy in purchasing parity terms in 2050. By then it expects China will be number one and the U.S. third.

India has 1.35 billion people, of which two-thirds are under the age of 36, so the narrative is the broader emerging market story of a young population with rising income and spending power. As living standards rise, the country will eat better, dress more fashionably, form households, and raise families. Indians will use more Internet and cell phone services (already world leading), look for more forms of entertainment, travel more, and dine out. The World Bank says this transition is well on the way and India will soon be joining the new global middle class.

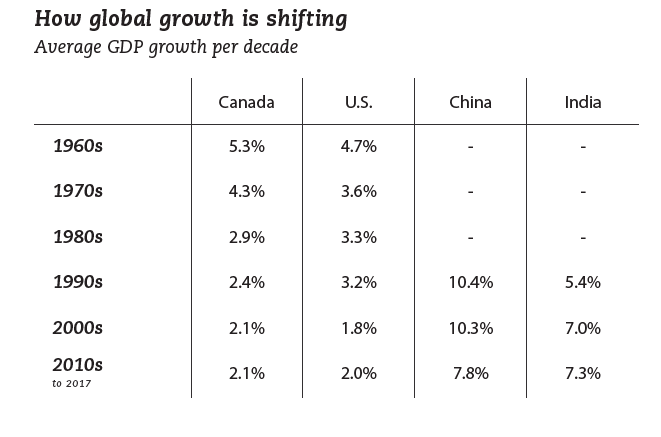

India will progress in fits and starts and not all of its promise will be realized. But this year, it became the fifth largest global economy, having bumped the U.K. into sixth. In 2018, economic growth is expected to average 7.4%, a global best.

India has three energizers at work. There is a demographic dividend created by a young and increasingly urban population. There is a democratic dividend, where the tools of a parliamentary democracy move the country forward by blending social and economic needs with the rule of law in a way that China cannot. These forces are a catalyst for the third energizer, which is rising demand for consumer goods and services.

India is perhaps a decade behind China in its development, with per capita income about a quarter of China’s. The two are often compared, but they are quite different. In India, business is conducted in English and the legal system is based on English common law. China is a one-party communist state where business is conducted in Mandarin, although English has become more prevalent. State ownership is pervasive and dealings are not always transparent.

I visited India to research a book about investing in emerging markets. At a briefing in Mumbai, Samiran Chakraborty, chief economist for the Citi banking group in India, talked about the speed at which India is changing.

He noted that it took 35 years between 1965 and 2000 for Indian GDP per capita to rise from US$100 to $500. It took six years between 2000 and 2006 for it to double and another six to grow by a further 50% to $1,500. He projects that in four years per capita GDP will exceed $2,500. This is an important number because in purchasing parity terms it means India is a lower middle-income economy. It is at this point that consumption lifts off.

Here are some trends:

- About 1 million Indians enter the workforce every month. While two thirds of the population is under the age of 36, fully 50% is under age 25. So half the country is entering the high consumption years that include marriage, household formation, and families.

• Much of this growth will be in cities. India is still a rural country, but its urban population is growing quickly. A third of Indians live in a city, a portion that is expected to rise to 50% in 20 years. Urbanization allows the efficient movement and distribution of goods and services. - Internet and cell phone use is high, but e-commerce transactions are very small. India had 462 million Internet users in 2017, second only to China. (Canada has 30 million.) The number of Indians with a cell phone reached one billion in 2015. Yet with a population 30 times that of Canada, India conducted just a quarter of our e-commerce transactions. That means enormous potential for banking and financial services.

- There are big gains ahead for basic consumer durables. Under 10% of the population owns a washing machine and only one in five households has a fridge.

The Narendra Modi government wants to keep the economy expanding to create jobs. His policies include spending on affordable housing, upgrading roads, modernizing rail networks, building rapid transit links, and investing in clean water, power, and telecom.

The plans for the Delhi – Mumbai corridor give a taste of India’s ambitions. The plan is the largest infrastructure project in the world with an estimated cost of US$100 billion. The work includes a 1,500 kilometre, six-lane expressway linking the two cities.

Alongside the highway will be a dedicated freight rail corridor. There will be two power plants, 24 smart cities with industrial hubs, and six airports in between the two cities. The goal is to reduce from two weeks to 18 hours the time needed to transport goods from Delhi to India’s west coast.

Modi has tackled corruption and tax evasion in several ways. In November 2016, with the utmost secrecy, the Reserve Bank of India removed all small rupee notes and printed billions in new ones, which were distributed throughout the country overnight. You could exchange old bills for new, but if you didn’t have a bank account, one would be opened and linked to your social insurance number. Instantly, billions of taxable rupees entered the system.

Modi has moved to the direct deposit of pensions and other social payments. Cash no longer passes through many hands before making it to the recipient with ‘handling fees’ deducted along the way. A national Goods and Services Tax (GST) is replacing 12 individual state taxes. It simplifies the tax regime and unifies India as a common market.

India is in transition where things are improving, but not at the same time. Sometimes it appears nothing is happening, as one initiative moves forward while another one stalls. But as the world’s largest emerging market, it’s a matter of when, not if.

The investments recommended below offer different ways to capture India’s prospects. One is via a Canadian multinational with a long history in Asia. The other is a more narrowly focused ETF, which is capturing India’s consumer potential.

Sun Life Financial (TSX, NYSE: SLF)

Background: Sun Life Financial is Canada’s third-largest insurance company by market capitalization ($29 billion). It provides a range of financial services including life, health, and travel insurance plus financial advice and pension and wealth management.

It is an old Asia hand and sees the region as the key to growth. Sun Life opened its doors in India in the 1890s and was India’s largest non-Indian insurer by 1956 when the industry was nationalized. Sun Life re-entered the market in 1992.

Sun Life Asia operates in seven Asian markets including India, China, Hong Kong, the Philippines, and Malaysia. In its latest quarter to June 30, the Asian unit accounted for 15% of profits. CEO Dean Connor said in an interview with Reuters that he expects to double profits in Asia over the next five years.

Performance: The shares touched a 52-week low of $47.55 last week before rebounding slightly.

Recent developments: In its second quarter, to June 30, Sun Life beat expectations earning $729 million, a 5.8% increase from a year earlier. Earnings per share rose 7.1% to $1.20 because of fewer shares outstanding. As of June 30, it had $986.1 billion in assets under management.

Acquisitions: In December 2017, Sun Life acquired Toronto’s Excel Funds, a mutual fund company with a 20-year history in emerging markets. Excel’s niche was India, although it offered a wider emerging market mix. Excel had $700 million in assets under management at the time of its sale, dominated by its flagship India Fund.

Excel’s funds have been rebranded under the Sun Life Global Investment flag. Through Excel, Sun Life strengthens its relationship with the Aditya Birla Group, one of India’s largest conglomerates. Birla managed the funds for Excel and is also involved with Sun Life in a broader Indian wealth management partnership.

Dividends and buybacks: Sun Life has increased its dividend twice in the past 12 months. The most recent was a 4.7% increase effective with the June payment. The current $0.475 cent quarterly dividend ($1.90 annually) yields 3.85%.

During the first half of 2018, SLF Inc. purchased and cancelled approximately 3.8 million common shares at a total cost of $206 million. During 2017, the company purchased and cancelled approximately 3.5 million common shares at a total cost of $175 million.

Outlook: Sun Life should also benefit from rising interest rates. Insurance companies invest the premiums from policyholders in fixed-income securities. As rates rise, they earn more on these investments.

Sun Life closed at C$49.34, US$37.61 on Friday ( Oct. 19) near its low for the year and 12% below its 52-week high of $56.09. The weakness provides an opportunity. The price-to-earnings ratio is a reasonable 12.6.

BMO India Equity Index ETF (TSX: ZID)

Background: This ETF tracks the performance of 15 Indian stocks traded as American Depository Receipts (ADRs) and Global Depository Receipts (GDRs) in New York and London. The 15 are blue chips, among the biggest and most financially stable Indian companies.

Chris Heakes, director and ETF portfolio manager for BMO Global Asset Management, says the ETF has $260 million in assets, is passively managed, and rebalanced each quarter. He says the ETF has held up well in the climate of rising U.S. interest rates and trade tensions because it holds the strongest of India’s emerging multinationals. He says it is suitable for more aggressive investors who can accept emerging market volatility and take a longer tern view.

Performance: This ETF has indeed performed well against its peers. It closed Friday at $22.60. As of the time of writing, it was down about 4% year-to-date. The Excel (Sun Life Financial) India Fund was down 16.4% and the New York traded iShares India Index ETF was down 8.3%.

Holdings: The better performance can be attributed to the fund’s weighting towards banks, technology, and consumer stocks. The ETF has 38% of holdings in four Indian banks: ICIC, the State Bank of India, HDFC, and Axis. Another 13% is held in conglomerate Reliance Industries, which is involved is everything from energy and textiles to retail and telecom. Larsen and Toubro (11%), a CPPIB partner, is India’s largest engineering firm. Three multinational technology stocks – Infosys, Wipro, and WNS holdings comprise another 20%.

Key metrics: The management expense ratio (MER) of 0.73% is on the high side. The dividend yield is 0.37%, paid annually. The fund was launched in January 2010.

This is ETF is attractive for those who can tolerate more risk and accept the volatility that comes with emerging market investments. The current price is $22.60.

This article first appeared in the Oct. 22, 2018 edition of the Internet Wealth Builder Newsletter.

Also read: Safe ways to invest in emerging markets

0 comments on “The Future is India”