The sun has been shining on shares of solar energy companies this year as a coming of age of the technology and converging trends have heightened interest in the industry.

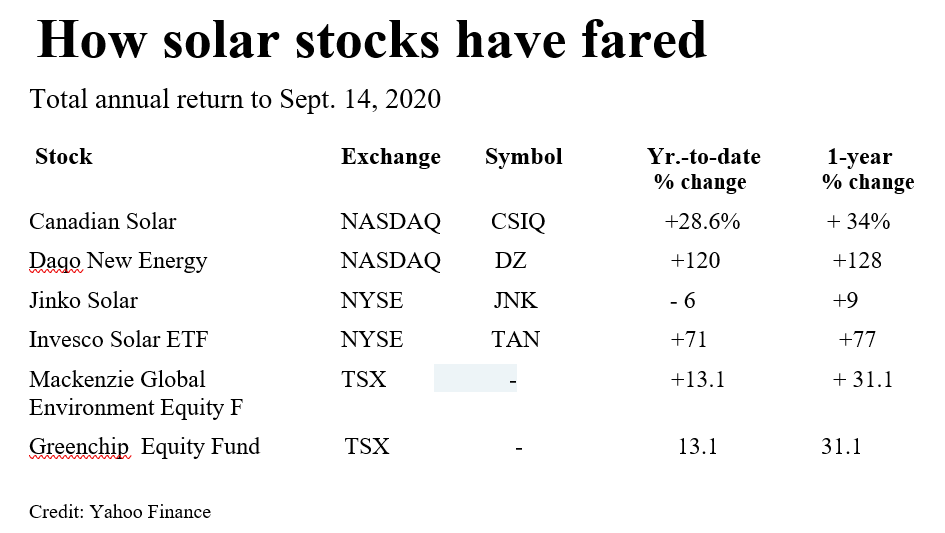

Case in point: The US$ 1.3 billion Invesco Solar ETF, (NYSE:TAN) which is a good proxy for the sector, is up 62% year-to-date as of early September and 130% since its mid-March low. That compares to the S&P TSX Composite index, which is down 4.95 per cent in the same period.

“Solar energy is a poster child for the life cycle of a new industry,” says Jason Bloom, Global Macro ETF Strategist with Atlanta-based Invesco Ltd. “We had sky high hopes 10 years ago but everyone was wrong about the profitability timeline. Now we have reached maturity.”

Mr. Bloom and John Cook, CEO of Greenchip Financial Corp., a Toronto-based green investing pioneer, say several forces are behind the trend. Two decades ago, solar was a new technology going through a rapid evolution and dependent on subsidies to make economic sense. The industry no longer needs that support and technological advances have evolved to make solar the cheapest source of power in some parts of the world.

“Growth is going to be way bigger than people think,” says Mr. Cook, who believes we are in the early stage of an historic transition away from fossil fuels. “Even after this year’s gains there is value to be found.”

Greenchip’s Global Equity Fund has $130 million in assets as of Aug. 31 and is mostly owned by pension, endowment funds and corporations. Greenchip subadvises the Mackenzie Global Environmental Equity Fund which has the same holdings, but with a smaller minimum purchase. The Mackenzie fund has $113 million in assets as of Aug. 31.

Greenchip holds all renewables, not just solar, as well as technologies that improve energy efficiency. Solar and related components are about 19 per cent of the fund.

The Invesco ETF has 100% of its holdings in solar and solar equipment and the strategies differ. About half of the Invesco ETF’s holdings are in the U.S., with roughly a quarter each in Asia and Europe. Greenchip’s allocation is reversed – 40 per cent is in Europe, followed by 23% in Asia and 17% in the U.S.

Mr. Bloom believes that China-based companies excel at the cheap manufacturing of solar panels but aren’t as good at making the equipment that controls power plants. This include inverters, which are the brains of the systems and monitor and manage solar arrays. North American companies offer superior quality, he says.

“Chinese inverters tend to be less sophisticated and less reliable,” Mr. Bloom says. Both Mr. Cook and Mr. Bloom agree that the move by a handful of players, already listed in New York, to seek a dual listing in China, has helped push up share prices.

“Investors are looking at these companies with fresh eyes and seeing that they are cheap relative to their assets and prospects. That’s given the stocks a huge lift,” Mr. Cook says.

Canadian Solar Inc. (NDQ:CSIQ), based in Guelph Ont., is part of the dual listing trend. It has been on the Nasdaq exchange since 2006 and in July said it is seeking a listing on the science and innovations board either in Shanghai or Shenzhen. Its shares jumped 8 per cent the day of the announcement.

JinkoSolar Holding Co. Ltd., (NYSE:JKS) the world’s largest manufacturer of solar panels, listed in New York in 2010. It was added to the Shanghai Stock Exchange’s Science and Technology Innovation Board in May. Daqo New Energy Corp. (NYSE: DQ) is another. Daqo makes polysilicon which companies like Jinko and Canadian Solar use to make panels and has announced its intent to list in Shanghai.

Mr. Cook says the dual listings have put the sector in a spotlight which has helped create new perceptions of value of the companies.

For example, he says Canadian Solar has evolved from a company making solar panels to one with a growing business building solar power plants for utilities and large power users. It closed the sale of a Japanese plant this winter and has since signed commitments for two more each in Texas and Brazil.

Yet, the value attributed to Canadian Solar is mainly from its solar panel business, Mr. Cook says, ignoring the power plant potential. In its latest reporting period, Canadian Solar beat estimates for revenue and earnings but its price to earnings ratio of its shares sits at 8.

Solar has another edge when compared to other renewables, in that solar power plants are cheaper and faster to build than hydroelectric ones. This has made solar an increasingly attractive option for utilities who are under pressure from activists to replace fossil fuels with renewable power.

“This trend is a huge tailwind,” Mr. Bloom says, “In Europe and the U.S. where there is a huge focus on reducing pollution and carbon emissions, you have a conviction among asset managers that this is the way to go. It is forcing the transition.”

Favourable government policy globally is another push. This includes the US $3 trillion green energy plan of U.S. presidential challenger Joe Biden.

Mr Bloom says investors should keep an eye on other renewables, including hydrogen fuel cells. He believes they are a better bet for heavy transportation than the lithium-ion batteries used in electric cars.

“Lithium-ion batteries are not in the future of long-haul trucking or aviation,” he says. “That’s because it means stopping too often to charge.”

And beyond current trends?

“There’s an operating power plant in China, that takes the pollution from a steel mill, feeds it bacteria and makes hydrogen,” Mr Bloom says. “That’s incredible. Green energy is coming in a lot of different forms. It’s a very exciting sector.”

This is an edited version of an that article appeared in the Globe Advisor section of the Globe & Mail’s Report on Business on Sept.15, 2020.

so informative. But buying a Solar share in tesla is a good decision? or investing on something will be good.

LikeLike